UK growth rate beats expectations

Second quarter data released last month by the Office for National Statistics (ONS) confirmed that UK economic growth did slow between April and June after an unusually strong expansion during the first three months of the year.

According to the latest official statistics, UK economic output rose by 0.3% across the whole of the second quarter. However, while this figure did represent a significant slowdown from a first quarter growth rate of 0.7%, it was notably higher than economists had been predicting with the consensus forecast from a Reuters poll pointing to growth of just 0.1%.

This stronger than expected performance was partly due to upward revisions to data in the first month of the quarter, with updated figures showing that, rather than contracting by 0.3%, output in April actually fell by a more modest 0.1%. The economy also performed better than analysts had been expecting in the quarter’s final month – output in June was estimated to have risen by 0.4%, driven by growth across all three main sectors of the economy.

Survey evidence also points to a more recent pick-up in activity. Last month’s preliminary headline growth indicator from the closely-watched S&P Global UK Purchasing Managers’ Index (PMI), for instance, rose to 53.0 in August, up from a final reading of 51.5 in July. This was the highest figure since August last year and left the index comfortably above the 50 threshold that denotes growth in private sector output.

Commenting on the findings, S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said the data indicated that “the pace of economic growth has continued to accelerate over the summer after a sluggish spring.” He did though add a note of caution by stating that the survey’s measure of order books highlight both an “uneven and fragile” demand environment.

Interest rates cut after narrow vote

On 7 August, the Bank of England (BoE) sanctioned a further quarter-point cut in interest rates, taking the cost of borrowing down to its lowest level for more than two years.

The decision, however, did require an unprecedented second vote after a first round of voting revealed a three-way split amongst policymakers on the BoE’s nine-member Monetary Policy Committee (MPC) – four of the members preferred to leave rates unchanged; four favoured a 0.25 percentage point reduction and one backed a half-point cut. The second vote produced a 5-4 majority in favour of cutting rates by 0.25 percentage points taking Bank Rate down to 4%, its lowest level since March 2023.

Speaking after announcing the committee’s decision, BoE Governor Andrew Bailey reiterated his view that the path for interest rates “continues to be downward” but added that it was important rates were not lowered “too quickly or by too much.” He also admitted that the decision to cut rates in August had been “finely balanced” and that the course of future cuts has become “more uncertain.”

The tightness of the MPC vote and clear differences in policymakers’ opinions did result in some economists suggesting the pace of any future rate cuts may slow over the coming months. Investors also interpreted the decision this way, trimming their bets on the possibility of another cut this year, with interest rate futures contracts only fully pricing in a reduction to 3.75% during the first quarter of 2026.

A Reuters poll conducted in mid-August though did show that a majority of economists currently still expect the Bank to cut rates one more time this year, with November viewed as the most likely date. The next MPC meeting is due to conclude on 17 September with the committee’s decision scheduled to be announced the following day.

Markets

At the end of August, the FTSE 100 and European indices faltered, with US indices also weaker, as markets digested an update on consumer inflation in the States which showed prices remained stubbornly above the Federal Reserve’s target.

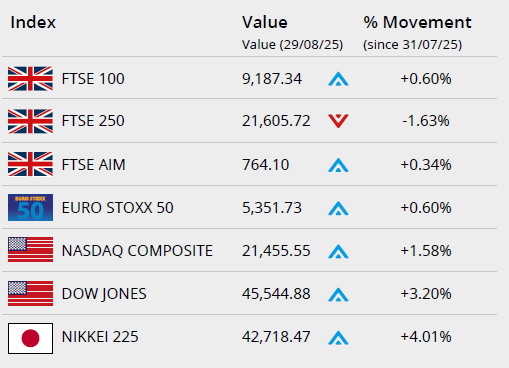

On home shores, the blue chip FTSE 100 closed the month on 9,187.34, a small gain of 0.60%. The mid-cap FTSE 250 lost 1.63% in August to end on 21,605.72, while the small-cap orientated FTSE AIM registered a small 0.34% gain to close August on 764.10.

In the US, the Dow Jones closed the month on 45,544.88, an uptick of 3.20% in the month, while the tech-orientated NASDAQ closed the month up 1.58% on 21,455.55. On the continent the Euro Stoxx 50 rose just 0.60% during August to 5,351.73. In Japan, the Nikkei 225 gained just over 4% to close the month on 42,718.47, with the US trade agreement and corporate reform providing support.

On the foreign exchanges, the euro closed the month at €1.15 against sterling. The US dollar closed at $1.35 against sterling and at $1.16 against the euro.

The gold price rose 4.82% during August, closing at around $3,509 a troy ounce. The price reached highs at month end, supported by heightened expectations of a September rate cut, as traders digested US economic data. Brent Crude closed the month at around $66 a barrel, recording a loss of over 6%. The price faltered at month end as traders digested weaker demand in the US and an autumn supply boost from OPEC and its allies.

Inflation rises to 18-month high

Official consumer price statistics released last month revealed another jump in the headline rate of inflation, while survey data points to a further, more recent rise in food inflation.

The latest ONS data showed that the Consumer Prices Index (CPI) 12-month rate – which compares prices in the current month with the same period a year earlier – stood at 3.8% in July. This was up from 3.6% in June and slightly higher than the consensus prediction from a Reuters poll of economists.

ONS said transport costs, particularly air fares, were the largest upward contributor to July’s rise. In addition, the cost of food and non-alcoholic drinks increased for the fourth month in a row, with prices in this sector rising to 4.9% in the year to July, the highest recorded figure since February 2024.

Survey data subsequently published by the British Retail Consortium also found that food prices continued to rise in August, while Ofgem’s recent decision to increase its gas and electricity price cap by a slightly higher than expected 2% from October will further add to consumer cost pressures. The BoE updated its inflation forecast early last month with the headline rate now expected to peak at 4% in September.

Government borrowing lower than expected

Although the latest public sector finance statistics revealed that UK government borrowing came in below expectations, the Chancellor is still expected to have to raise taxes in the Autumn Budget to meet her self-imposed fiscal rules.

Data released last month by ONS showed government borrowing in July totalled £1.1bn; this was £2.3bn less than the same month last year and the lowest July figure for three years. The better-than-expected data was helped by an increase in self-assessed Income Tax receipts, as well as a rise in National Insurance (NI) payments due to April’s employer NI rate hike.

July’s figure took cumulative borrowing across the first four months of the financial year to £60bn. While this was £6.7bn higher than in the same period last year, it was broadly in line with the Office for Budget Responsibility’s latest forecast produced in March.

Economists, however, still expect that the Chancellor will need to raise taxes this autumn if she is to meet her borrowing rules. Analysis released early last month by the National Institute of Economic and Social Research, for instance, estimated that the government is likely to miss its budget target for 2029/30 by over £40bn.

All details are correct at the time of writing (01 September 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.