Looking ahead

We use our in-house cash flow planning tool, Voyant, to take all that we know about your current financial situation and project forward your financial position.

The purpose of our cash flow planning process is to provide an interactive way of projecting your financial future at different life stages, to give you more clarity and peace of mind. Whilst the cash flow forecast serves only as an indication of the future, it can be very useful in providing answers to questions to help you achieve financial empowerment. Examples of these include:

- Can I afford the costs of private education for my children or grandchildren?

- How much do I need to save to meet my future retirement spending goals and how much investment risk do I need to take?

- What would be the impact on my long-term financial position if I retired early?

- Can I afford to spend more in the earlier years of my retirement and how would this impact my family in later life?

- Can I afford to gift money to my family to help secure their future, whilst mitigating the impact of inheritance tax on my estate?

- Can I afford the costs of long-term care in later life?

To build your cash flow plan, we require a full overview of your financial position as this allows us to be as holistic as possible. Therefore, it is important for us to get a full understanding of what you want to achieve in the short, medium and longer term.

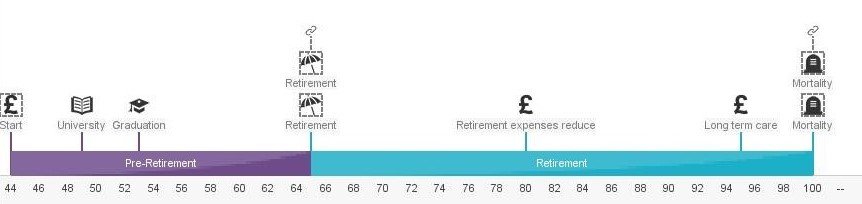

The first step is to produce a timeline of key events in the future. Typical examples of these include your future retirement dates, possible downsizing in retirement to release equity and an assumed date for entering long-term care. However, we can expand out to more specific future events and examples of these include one-off expenses for family weddings, house deposits, planned one-off holidays and education costs. An example timeline is shown below.

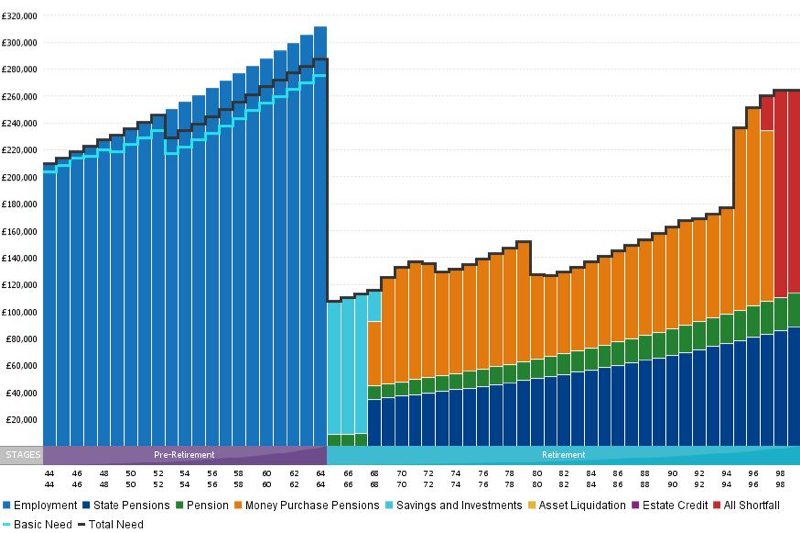

The next stage is to produce a cash flow forecast, which projects your cash inflows (salary, pension and investment income) and outflows (normal expenses, planned savings and taxation) for each year during your lifetime. This allows us to identify any shortfalls and to design a strategy that enables your affairs to be structured as tax efficiently as possible, helping to preserve the overall sustainability of your asset base during your lifetime. An example cash flow forecast is shown below.

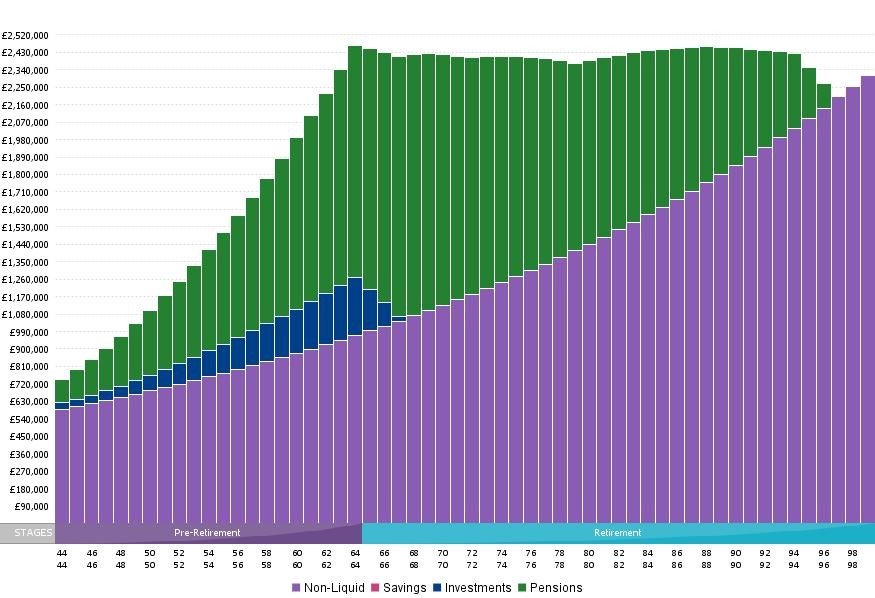

Finally, we produce an asset projection which analyses your overall asset base throughout your lifetime. This provides us with an overview of how your asset position will differ over time and can be particularly useful when making decisions around structuring investments tax efficiently and protecting your estate against the impact of inheritance tax. An example asset projection is shown below.

Once the above process has been completed, we will issue a summary report to you which details our findings and our suggested course of action for you going forward. This will also confirm the assumptions we have made concerning future investment growth, inflation and taxation.

Our natural approach is to be conservative in the assumptions that we use. This is vitally important when projecting into the longer term, as unrealistic assumptions (on future growth rates and inflation, for example), can lead to sub-optimal decisions being taken today. This, when combined with regular updates to your cash flow plan, enables us to ensure our advice adapts to your changing needs and your financial arrangements remain appropriate on an ongoing basis.

Our typical approach is to review client cash flow plans on an annual basis in line with regular client review meetings. However, cash flow plans can also be requested on ad-hoc basis.